The renewable energy pool – answers to 13 concerns raised

In March 2023, the EU commission proposed a reform of the electricity market design (COM 2023/0077) to comprise a shift to the mandatory use of (two-way) contracts for difference (CfDs) as public support mechanism for investments in new renewable energy generation. The two-sided CfDs replace the one-sided support mechanisms that have insured renewable investors against potentially low power price developments in several member states, without providing a symmetric hedge for consumers against high power prices.

The initial proposal by the EU commission envisaged that “Member States should ensure ... [the conditions of CfDs] are passed on to all final electricity customers, including households, SMEs and industrial consumers, based on their electricity consumption.“ Granting proportional access to all consumers has many merits, but may need to be amended in the current situation allowing member states to flexibly provide preferential access to three consumer groups:

- Industry investing in transformational low-carbon technologies primarily based on electricity (or electricity-based hydrogen) could benefit from clarity concerning the affordability and availability of green electricity that is required to meet and contribute to global sustainability targets and standards.

- Neighbors of wind- and solar parks, to foster greater acceptance if they were granted access to electricity at affordable and stable electricity costs.

- Electricity intensive industry facing global competition could benefit from increased clarity on affordability and stability of electricity prices, thus limiting the need for alternative mechanisms to address concerns about international competitiveness.

To realize these opportunities, it has been proposed to pool CfDs tendered to non-dispatchable generation capacity (primarily wind and solar power) and to grant preferential access to this pool to consumers and electricity retailers on behalf of their consumers. Such proposals have been elaborated and analyzed in detail, for example in the discussion paper “Contracting Matters: Hedging Producers and Consumers with a Renewable Energy Pool”.

In the following part, we address 13 concerns related to the concept that have been raised in workshops with renewable investors, actors in electricity trading, utilities, industrial and private consumers as well as governments.

1. The number of beneficiaries would be small due to the initially limited sacle of RE pool, this could discriminating against others. keyboard_arrow_up

In principle, it is true that access to the Renewable Energy Pool (RE-Pool) to hedge electricity prices offers an advantage to electricity customers, as it reduces financing costs by avoiding regulatory risks and solving market failures in crises. The effective cost of electricity from wind and solar farms is thus reduced by around 30%. In addition, by using the existing reference yield model in the tender design, RE pools can avoid scarcity rents (e.g., land rents) at good wind sites, which leads to a further reduction in electricity costs.

For other electricity customers, there is no disadvantage compared to the status quo (the situation without an RE pool). With the Renewable Energy Pool, the government can support the industrial transformation and the transformation to a climate-neutral heating sector. Further, it can enhance acceptance of wind farms by specifically allocating a hedge via the renewable energy pool, without disadvantaging electricity customers or raising costs for the public sector.

2. Consumers outside the RE pool must expect higher prices if electricity supply to RE pool is removed from the market. keyboard_arrow_up

No, because the electricity generated by plants whose revenues are hedged with CfDs will still be sold entirely on the spot market. Compared to Power Purchase Agreements (PPAs), this has the advantage that the entire renewable generation is necessarily offered on the spot market, enabling efficient production, rather than possibly being optimized only within subsystems, as is the risk with bilateral PPAs.

3. If the state simultaneously acts as the sole buyer and seller of long-term contracts for new wind and solar energy, liquidity could be drained from the wholesale market. keyboard_arrow_up

This problem does not exist on the spot market as all generation is offered and sold there (see Answer 2).

The effects of remuneration mechanisms on forward markets have so far primarily been considered from the perspective of renewable energy producers, most prominently in the recent German reform that made the public budget, rather than electricity consumers, counter party to all support requirements and revenues from public support mechanism. This resulted in a lack of hedging instruments for electricity customers, as there was no incentive for renewable energies to offer their volumes on forward markets. This is different with an RE pool where consumers are hedged to the same extent as producers. In addition, there are incentives for electricity consumers and their suppliers to participate in the hedging market to hedge remaining risks:

By receiving shares in the renewable energy pool, customers have attractive electricity costs for the agreed energy volumes. Further, they are hedged against electricity price risks for the volumes corresponding to the generation profile of the renewable energies in the pool. At the same time, this creates an incentive for electricity customers and their energy suppliers to hedge against remaining profile risks - either by investing in flexibility or with forward market products. The introduction of the RE pool with a standardized generation profile, against which all customers are hedged, can catalyze the emergence of corresponding forward market products. This is necessary because without such a regulatory incentive and reference point, previous attempts to introduce flexibility products in the forward market have failed.

Thus, the introduction of an RE pool supports the development of forward markets and the participation of electricity customers in them.

4. Uncertainty relating to how government backed CFDs will be implemented creates uncertainty in the PPA market and risks delaying projects. keyboard_arrow_up

Such uncertainties, and reluctance to sign PPAs, will be induced by any discussions about regulatory developments. To avoid further delays of the necessary investments, it is important that clear decisions are made quickly now. In addition, current external developments, such as these of gas and electricity prices in the wake of the Ukraine war, cause risks to the realization of project pipelines. This could be addressed by quickly switching to CfD tenders for an RE pool.

5. Electricity supply contracts must match individual needs of electricity customers, not a standardized contract with an RE pool. keyboard_arrow_up

The renewable energy pool is not intended to replace the electricity supply contracts between energy supply companies (utilities) and consumers. Within the hedging portfolio of industrial consumers or utilities, the EE pool will complement forward contracts and PPAs with other generation technologies, existing plants, and wind- and solar plants involved in lifetime extensions. This ensures that electricity consumers and utilities have incentives to invest in flexibility and thus strengthen forward markets.

6. A RE pool prevents a rapid and market-based transformation of the industry as the electricity is no longer available for investments or PPAs. keyboard_arrow_up

PPAs remain an important hedging tool for generators and electricity customers. For example, PPAs have been and will continue to be used to hedge investments for plant lifetime extensions. They will also continue to be central to generation technologies with fuel costs, such as biogas, etc.

However, the role of PPAs is limited by the ability of buyers to enter long-term contracts and to hedge political risks in electricity markets. According to our analyses, the necessary expansion of wind and solar energy can be undertaken more quickly and cost-effective with the help of an RE pool. Of course, this requires a change in some business models, especially of the actors currently involved in the design of PPAs of wind and solar projects. Policymakers must create a clear framework for the market-based transformation such that that business models previously based on PPAs can evolve quickly.

7. If electricity market prices fall below the competitively determined price of the CfD tenders, electricity customers in the RE pool are obliged to make additional payments to their spot market costs. keyboard_arrow_up

This is in the nature of hedging instruments and occurs in the EE pool just as it does in bilateral PPAs. Hedging allows electricity consumers to avoid exposure to high electricity costs at the expense of higher electricity costs than pure spot price-based procurement would offer in low-price periods.

8. In some countries, auctions of sites for wind farms have resulted in high proceeds. These funds could be used to finance grid and reduce grid fees. keyboard_arrow_up

The payments by renewable producers demonstrate how valuable renewable electricity can be to society and how scarce suitable sites are. Scarcity rents can be partially captured through license tenders, but since future revenues are uncertain, they are heavily discounted and hence only a fraction is passed-on to customers.

These scarcity rents can also be captured in the RE pool, for example through CfD tenders for specific areas or by reflecting a resource differentiation in the auction design (like it is common in the reference yield model in Germany). They are then passed on, undiscounted, in the form of reduced hedging costs. In addition, the RE pool has the advantage that the better risk profile can reduce the costs for end customers by 30% compared to a PPA approach.

9. CfD tenders provide insufficient incentives for system friendliness of installations. keyboard_arrow_up

Tenders for the sliding market premium use a monthly reference period to incentivize the choice of system-friendly solar panel orientation (west/east, where appropriate) and wind turbine design (larger rotors relative to generator capacity). A more system friendly design will increase the share of production in periods with less renewable generation and thus allow the investors to benefit from the higher electricity prices during such periods. The benefit of system friendly installations will increase in the coming years. But as these benefits are uncertain, they are discounted quite heavily in financing and are therefore smaller than desirable from a systems perspective.

CfD tenders could already include the incentives for system-friendly alignment in the tender design. A bonus could be calculated for system-friendly plants (i.e., east/west orientation or rotor/generator ratio) - analogous to the current reference yield model - which is taken into account, when ranking the incoming bids. Ultimately, this results in system-friendly plants being successful in the tenders, even if they have higher bid prices. In this way, the full incentives for system-friendly investments can be ensured.

With such a bidding design, system friendliness can be incentivized while reducing the reference period to one (quarter) hour. This allows a design of the contracts in which the plants react to the spot price during operation, i.e., stop production when electricity prices are negative.

10.The CfD auctions for an RE pool do not incentivize electricity storage. keyboard_arrow_up

In the past, some auctions incentivized joint investments in wind/PV plants and associated electricity storage. This was certainly due to a lack of support programs for storage, and thus an attempt to allow initial experience with storage. The task now is to develop an efficient market design for RE generation and storage. It should be possible for market participants to realize storage and wind or solar projects separately. This allows a larger group of market players to participate and contribute with their experience and innovations, thus strengthening competition. It also ensures that both RE generation and storage are operated in a system-oriented manner.

Revenues from the spot markets, that are financially secured by CfD tenders or flexible forward products, offer an efficient framework. Should storage facilities at grid connections of wind or solar parks be necessary and economically viable, various options can be considered for such situations (tendering for storage by grid operators, etc.).

11. CfDs for an RE pool provide wrong incentives in times of negative prices. keyboard_arrow_up

Misaligned incentives in times of negative prices are not related to the RE pool instrument in general but depend on its design. There are several options that address these disincentives, e.g., production potential-based procedures that refer to calibrated readings in the plants and are already applied in balancing energy markets.

12. CfDs reduce the return on equity for investors. keyboard_arrow_up

CfDs reduce the risks associated with investments in renewable assets, so that overall, a lower total return is necessary to trigger investments. However, this does not necessarily mean that the return on equity also decreases, as lenders (e.g., banks) are willing to take larger shares of the investments. The leverage effect of the debt ratio can keep the return on equity just as attractive.

13. The proposal for an RE pool comes too late, most of the tenders for the next years have already run. keyboard_arrow_up

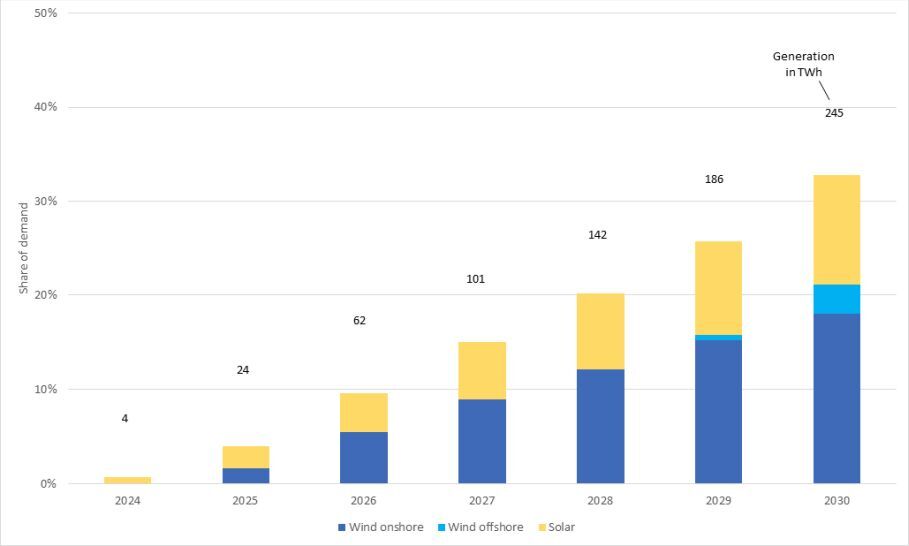

The government targets for wind and solar energy require, for example in Germany, the realization of projects that can generate 600 TWh of electricity in 2030 and, thus, cover 80% of electricity consumption in 2030 with supply from renewable energies.

If all tenders starting in 2024 were converted to CfDs, approximately 43% of the net addition of wind offshore, 80% of wind onshore, and 75% of solar generation from now to 2030 could be combined into an RE pool.The difference to 100% of the net additions for wind onshore and solar plants results from the fact that some of the plants that will be commissioned in the next few years have already participated in the tenders and are suppoerted under the old system of one-sided sliding premia, but have not yet been completed at the present time. In the case of solar energy, there is also a larger number of smaller plants (under 100 kWp) that do not necessarily have to feed electricity into the grid and receive a fixed premium should they feed in surpluses. Thereby, 245 TWh, or about one-third of the 750 TWh electricity demand expected for 2030, could be covered by the CfD pool.

These figures for the example of Germany show that with an adjustment of the support mechanism, a large part of the new construction could be supported with CfDs and combined in an RE pool.

Figure 1 Share of electricity demand by technology, that could be supported with CfDs until 2030 in GermanyWe assume that the expansion targets as determined in the EEG 2023 can be achieved. The shares are based on TWh figures calculated using capacity and number of full load hours. For new wind onshore plants 2500, for wind offshore 3900 and for solar plants 930 full load hours are assumed. The electricity demand is derived from the „Versorgungssicherheit Strom Bericht“ (https://www.bmwk.de/Redaktion/DE/Downloads/V/versorgungssicherheitsbericht-strom.pdf?__blob=publicationFile&v=4).