DIW Economic Outlook Spring 2025

Policy changes leaving marks on the economy

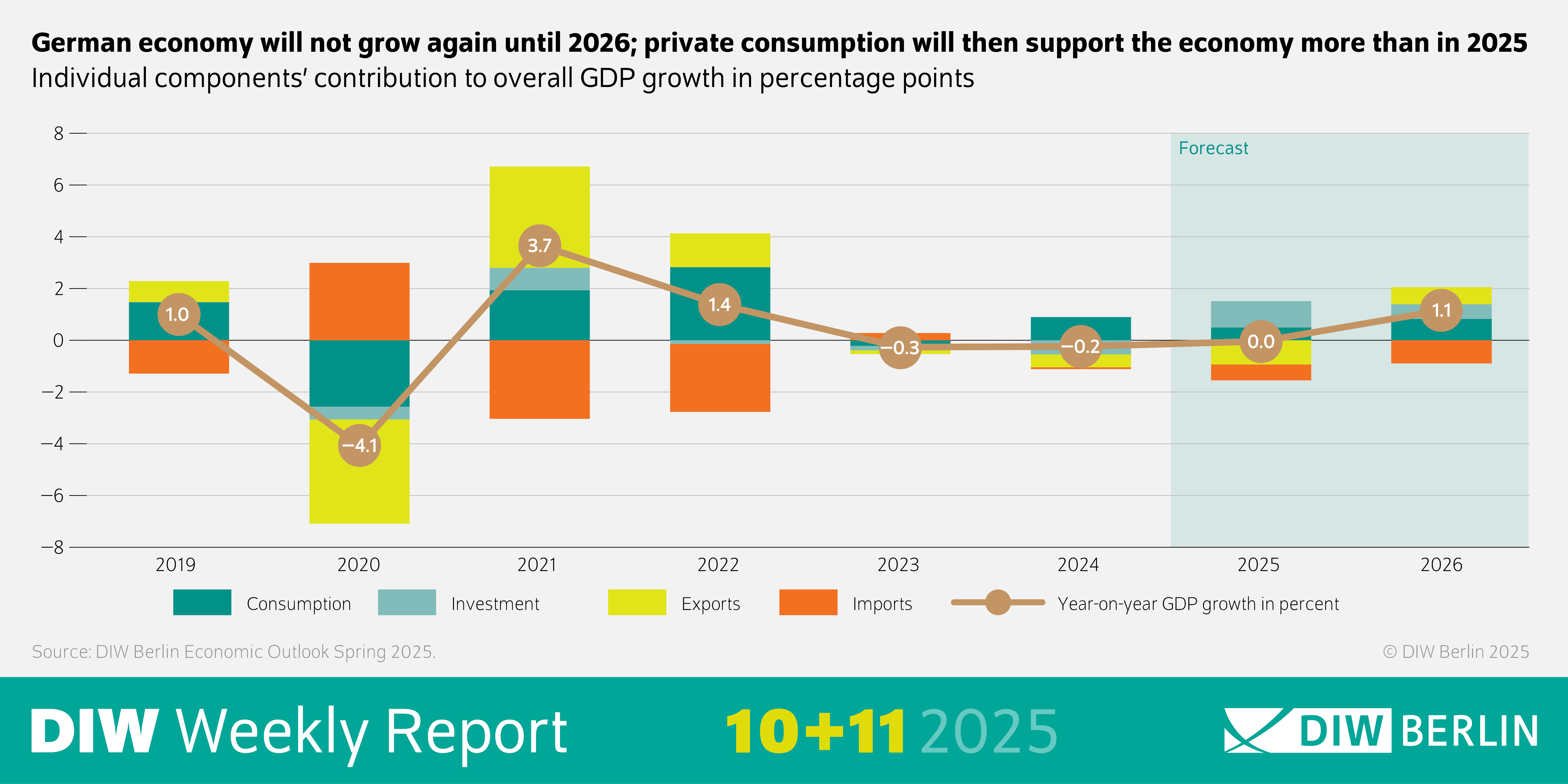

- German economy stuck in a period of stagnation; no average annual growth is projected for 2025, the third consecutive year

- Weak exports, growing unemployment worries, subdued private consumption, and economic uncertainty are slowing the economy

- Gradual recovery can be expected from summer if a government is formed, the labor market becomes more stable, and private consumption picks up speed

- Interest rate cuts support investments and a special infrastructure fund is planned; thus, economic growth should be around two percent in 2026 and at 1.1 percent without additional investments

- Global economy remains on track, even if US trade policy is having

© DIW Berlin

German Economy

German economy stuck in stagnation

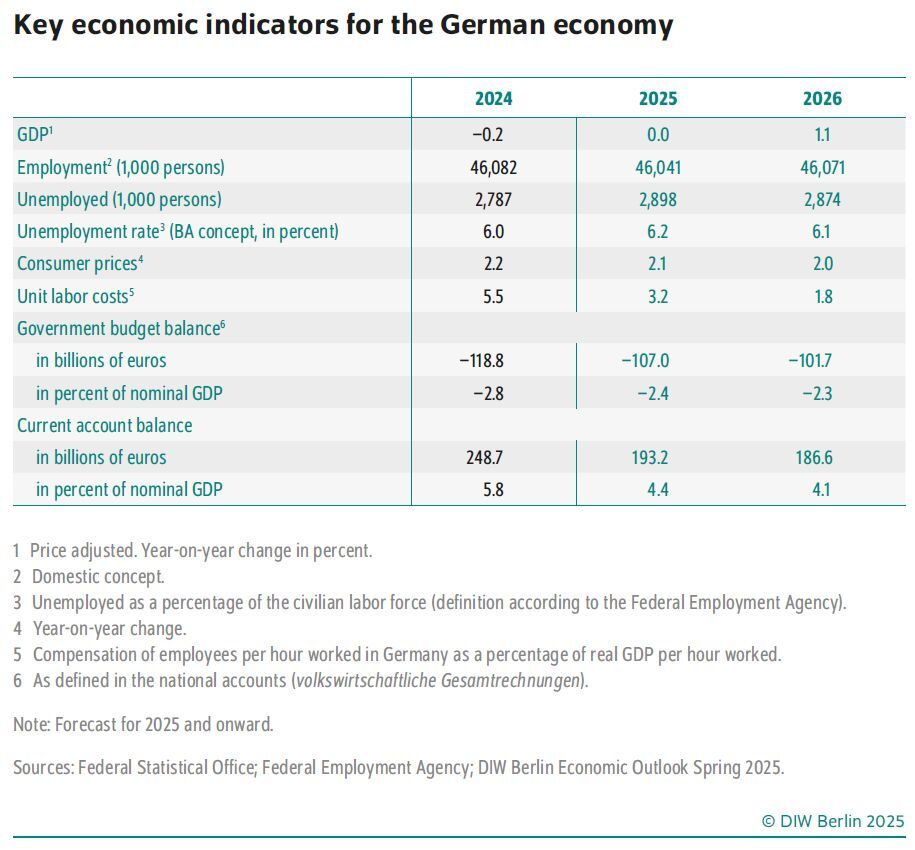

The German economy continues to stagnate and is likely to remain flat for the third consecutive year. Political uncertainty caused by the early federal elections, as well as global trade and geopolitical uncertainties, are affecting the German economy in a fragile situation. A significant recovery of 1.1 percent is not expected until next year. The German Institute for Economic Research (DIW Berlin) has therefore revised its economic forecast for Germany slightly downward once again. One of the main reasons for this is private consumption, which is developing more weakly than expected in Germany despite rising real wages. In view of the tense global political situation and concerns about job security, many people in Germany are holding back on major purchases.

“If the planned special infrastructure fund and the additional defense funds actually happen, they would be a game changer for German industry and a positive signal for industry-related companies.” Geraldine Dany-Knedlik, Head of Forecasting and Economic Policy Team

The end of 2024 brought a setback for German foreign trade. Demand from China and the United States declined sharply, hitting the automotive industry particularly hard. In 2025, broad stagnation is expected across nearly all sectors of the economy. Economic policy uncertainties are likely to slow down export activity in particular.

“Despite these challenges, there are also bright spots: with the brief exploratory talks and the coalition negotiations already underway, we can expect a functioning government to be formed quickly, which should also lead to greater clarity regarding the economic framework conditions,” predicts Chief Economist Dany-Knedlik. This is expected to further improve the business sentiment in the manufacturing sector, which has already brightened since last autumn, and to stabilize the labor market.

Although a slight increase in unemployment is anticipated for this year, the unemployment rate will remain at a comparatively low level. In 2026, employment is expected to rise again somewhat. Wages continue to develop positively, and inflation remains moderate. The inflation rate is projected to reach 2.1 percent in 2025 — slightly higher than forecast in winter — but should return to the European Central Bank’s stability target of two percent the following year.

More favorable financing conditions are also supporting the development of investment activity. Construction and equipment investment are likely to increase moderately, driven by rising demand from the public sector.

© DIW Berlin

Global Economy

Global economy braving times of political uncertainty

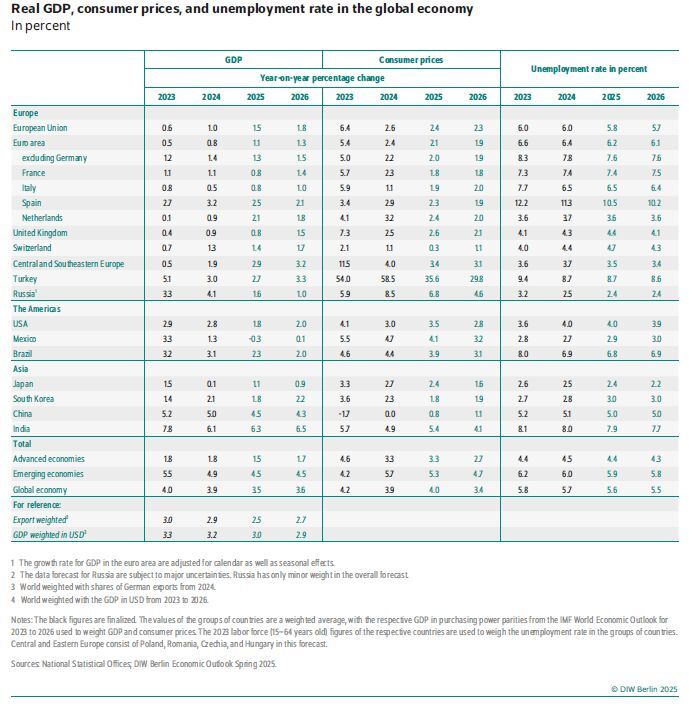

Germany is currently bringing up the rear among the major eurozone countries. Overall, the eurozone is likely to benefit from the customs asymmetries that still exist this year, as the EU is not yet as heavily affected by tariffs as China, Canada, and Mexico. Globally, however, the erratic trade policy of the US administration will leave a significant mark, particularly on world trade. Overall, despite rising trade barriers and uncertainty this year and next, the global economy is likely to grow at a rate not much lower than 3.9 percent in 2024. The fact that the rates are expected to be only 3.5 and 3.6 percent, respectively, is likely to be due primarily to a weaker US economy, which is suffering most from its own policies.

© DIW Berlin

{kind=link}