DIW Economic Outlook Summer 2026

Energy price shock slows German economy— Global growth remains moderate

- Energy price shock triggered by the Iran War stalls the nascent recovery of the German economy—technical recession expected around mid-year

- Deep downturn comparable to 2022/23 remains unlikely—shock is smaller, energy supply remains secure, and expansionary fiscal policy provides support elsewhere in the economy

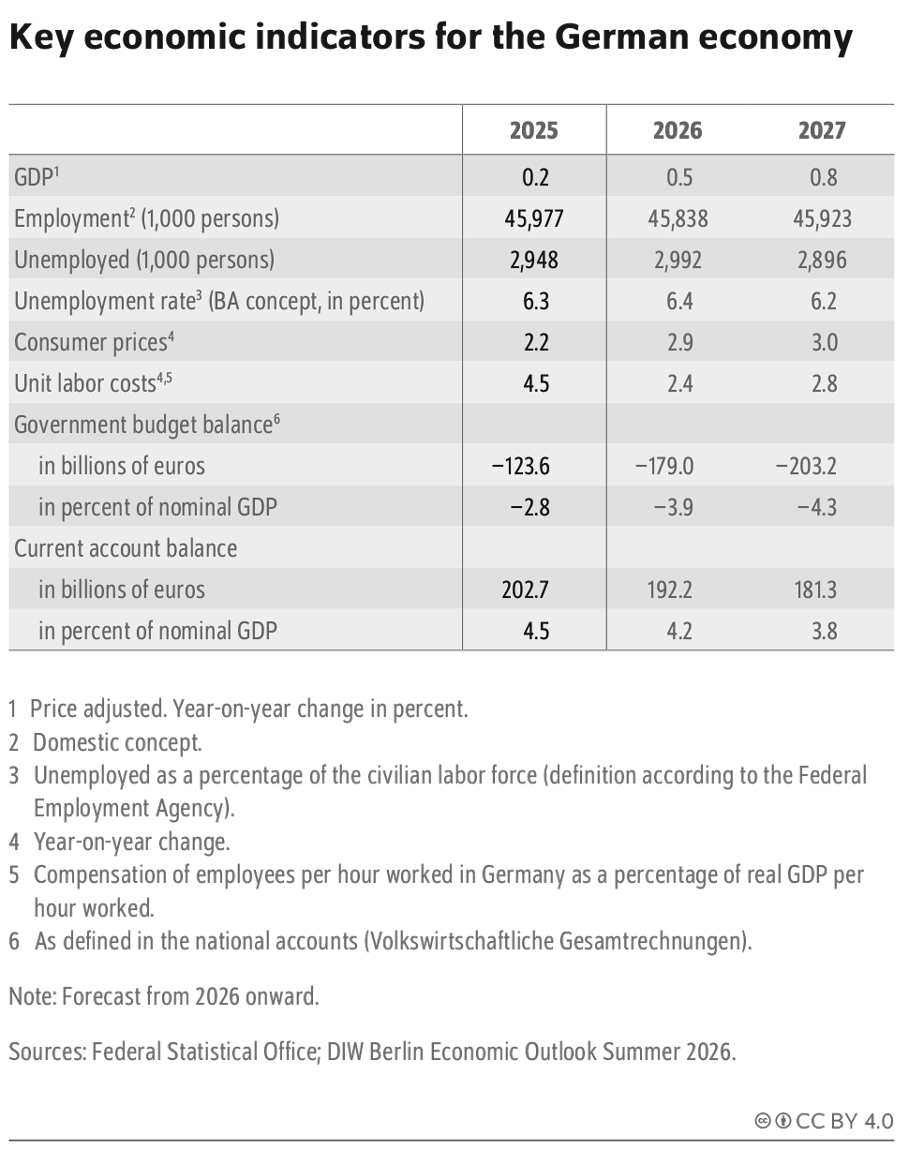

- Higher oil and gas prices push inflation to 2.9 percent this year and 3.0 percent next year— unemployment rate rises temporarily to 6.4 percent

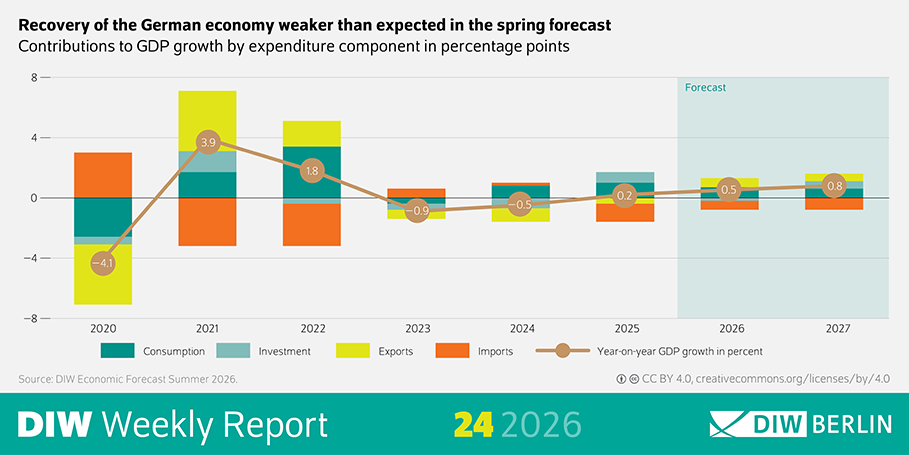

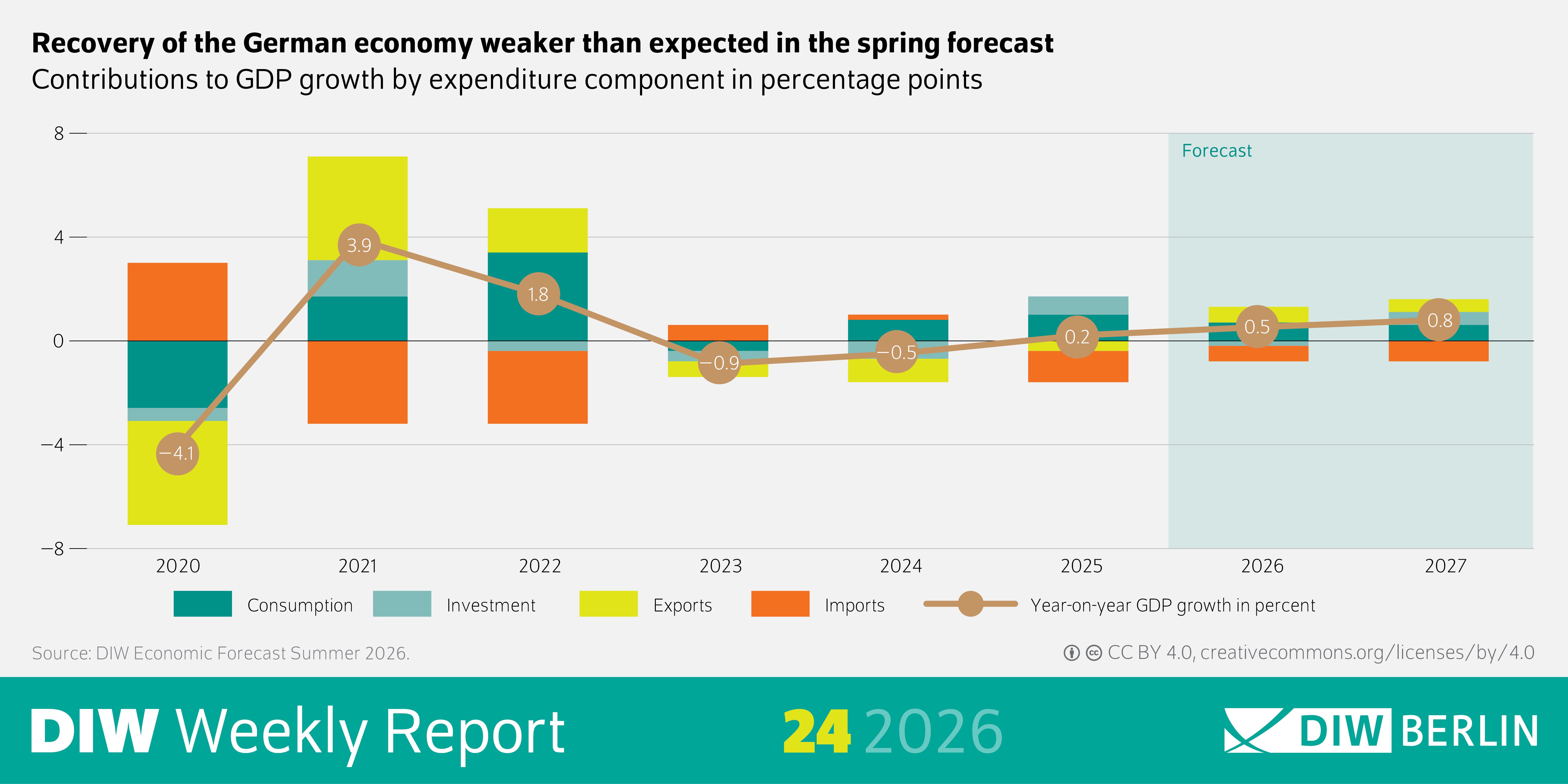

- DIW Berlin expects the German economy to grow by 0.5 percent in 2026 and 0.8 percent in 2027— forecast revised down by around 0.5 percentage points in each year compared with the spring outlook

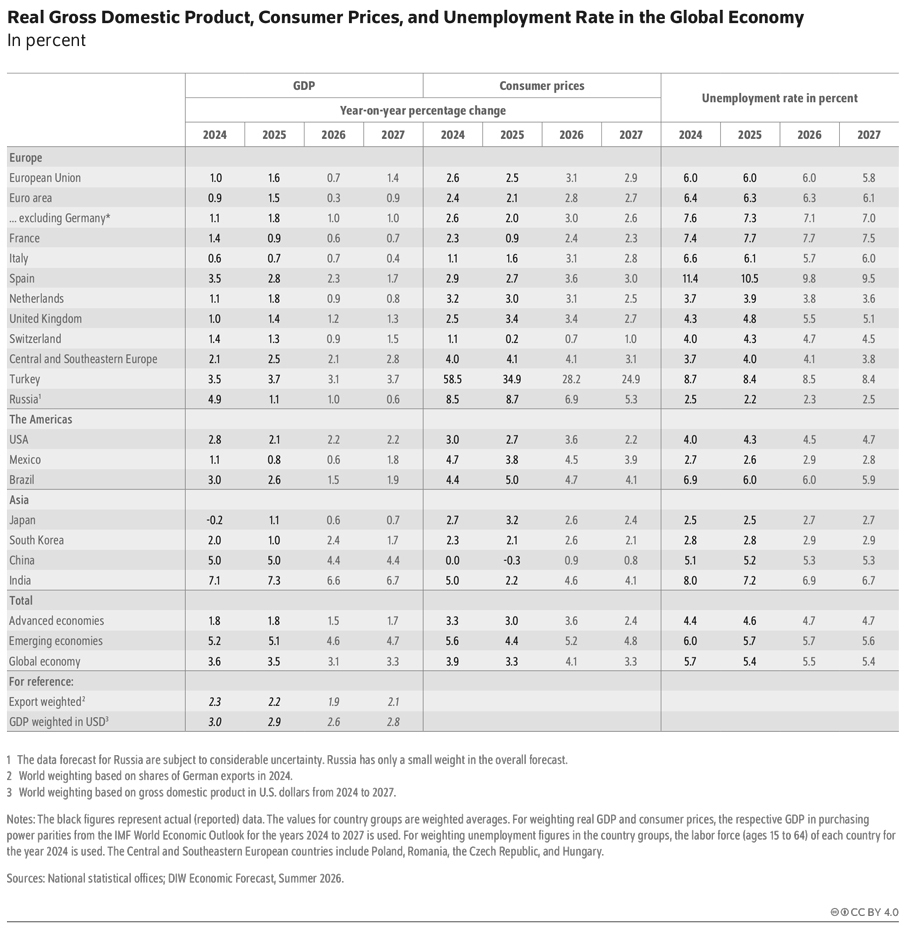

- Global economic output continues to expand at a moderate pace despite the energy price shock, by 3.1 percent this year and 3.3 percent next year—US economy continues to grow

German Economy

Energy price shock slows the recovery

The German economy is failing to gain momentum after three weak years. At the turn of the year, a modest recovery appeared to be taking hold, driven primarily by domestic demand and private consumption. However, in addition to the structural problems already present, the German economy must now also contend with the consequences of the Iran War. The energy price shock has halted the recovery before it could gain traction. Rising oil and gas prices have since been driving up consumer prices, eroding household purchasing power, and fueling the already widespread uncertainty. Nevertheless, a deep downturn comparable to the energy price crisis of 2022/23 does not appear to be on the horizon.

At the start of the year, Germany's economic output still grew by 0.3 percent, supported by the public sector and foreign trade, while the rest of the domestic economy remained weak. As the year progresses, the impact of the energy price shock is becoming clearly apparent: economic output is likely to contract slightly in the second quarter (by 0.2 percent) and decline marginally again in the third quarter, before stabilizing toward year-end. Private consumption is softening, and investment appetite remains subdued. Once again, the public sector remains the sole source of support. Even beyond the current year, the expansionary fiscal policy stance remains the decisive driver. Rising defense spending and the gradual deployment of funds from the special fund for infrastructure and climate neutrality will account for the bulk of growth—though they are no miracle cure, as the impact of these investments is unfolding only gradually.

After growth of 0.5 percent this year, DIW Berlin expects the economy to expand by 0.8 percent next year—both around half a percentage point lower than forecast in the spring outlook. Consumer price inflation, at 2.9 and 3.0 percent respectively, exceeds the European Central Bank's stability target, and the unemployment rate is rising to 6.4 percent this year. An updated scenario analysis by DIW Berlin highlights the scale of these risks. In a downside scenario derived from market expectations, growth this year would be around 1.5 percentage points lower—equivalent to the German economy contracting by just under half a percent in 2026. Inflation would reach a level similar to that seen during the energy price crisis of 2023.

“The German economy was only just starting to work its way out of a three-year slump when the Iran War drove up energy prices. This is noticeably slowing the recovery—but this is not a repeat of 2022: the shock is smaller, energy supply remains secure, and expansionary fiscal policy is providing support.” Geraldine Dany-Knedlik, Head of Division Forecasting and Economic Policy

Global Economy

Iran War Dampens Outlook for the World Economy—Yet Moderate Growth Expected

The global economy continues to grow at a moderate pace despite the energy price shock. While the Iran War is weighing on the global outlook, world trade expanded strongly at the start of the year and is only slowing modestly. The United States is bucking this trend, growing by 2.2 percent this year, driven by investment and energy exports; the euro area, by contrast, is growing only weakly at 0.3 percent. For global economic output overall, DIW Berlin projects growth of 3.1 percent this year and 3.3 percent next year.

{kind=link}